Over the last year we have seen an upswing in floating production and storage systems ordering after many years of low activity. According to our colleagues at World Energy Reports, āThe global oil and natural gas markets are contending with rebounding energy demand on top of supply disruptions from Russiaās invasion of Ukraine. As a result, activity and business sentiment in the floating production sector has seldom been strongerā¦

Asian liquefied natural gas (LNG) demand is projected to increase by 5% at 12 million tons (Mt) in 2024, following a 2% at 5 Mt growth in 2023, according to the most recent report by Wood Mackenzie.China, the worldās largest LNG import marketā¦

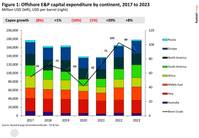

Ōʶ„¶Ä³”ĄĻ»¢»ś exploration and production (E&P) capital expenditures (capex) will shake off the pandemic-induced declines of the past two years and rebound by 20% in 2022, reaching a total $165 billion spent on exploration, wells, and facilities (Figure 1)ā¦

Demand for work-class ROVs (WROV) has traditionally been determined by the state of the global offshore oil & gas industry. This is likely to remain the case in the short to medium-term. However, thereās a new kid on the block ā offshore windā¦

Demand for work-class ROVs (WROV) has traditionally been determined by the state of the global offshore oil & gas industry. This is likely to remain the case in the short to medium-term. However, thereās a new kid on the block ā offshore windā¦

Over the past four months we have been flooded by news of just how badly the offshore rig market has been hit during the double whammy of the Corona pandemic and oil price fallout. We witnessed what seemed like a never-ending wave of contractā¦

The global heavy lift vessel market is a difficult place to be. Utilization for the fleet has remained depressingly low since the first oil and gas downturn in 2014, currently hovering around 33% for the global fleet with a lift capacity of over 800 tonnesā¦